Manila and Cebu Top the List of Southeast Asia’s Most Expensive Cities to Buy a Home

It's a global crisis.

by Kyzia Maramara | June 10, 2026

If it feels like owning a home has become a fantasy reserved for lottery winners and nepo babies, you’re not imagining things. For many millennials and Gen Z Filipinos, adulthood looks a lot like stretching money just a little further every payday. Homeownership is a distant dream. And with a new study ranking Manila and Cebu as the top cities in Southeast Asia with a homeownership crisis, that dream may indeed be getting farther out of reach.

Numbeo: Manila and Cebu rank among the world’s least affordable housing markets

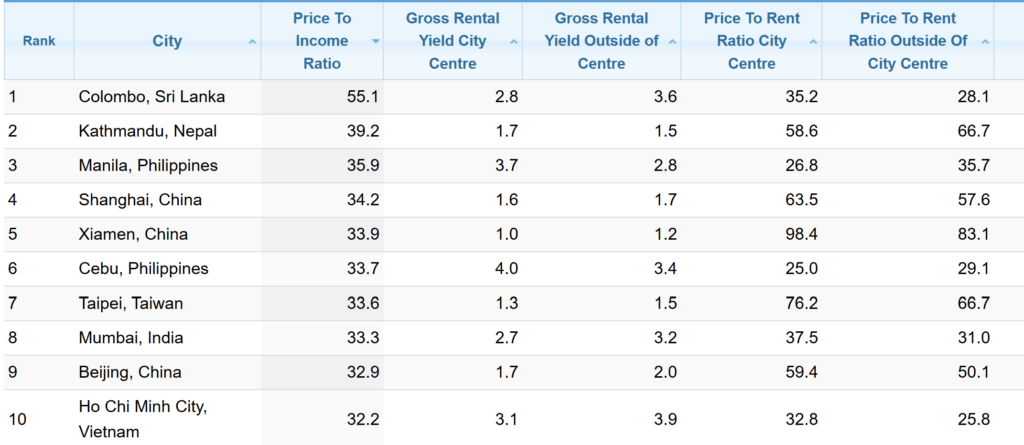

Numbeo’s Property Prices Index by City 2026 | Screenshot from Numbeo

According to Numbeo’s 2026 Property Prices Index, Manila ranked third worldwide for housing unaffordability, with a price-to-income ratio of 35.9. Cebu wasn’t far behind, landing in sixth place globally with a ratio of 33.7.

Only Colombo, Sri Lanka (55.1), and Kathmandu, Nepal (39.2), recorded worse scores than Manila.

Within Southeast Asia, the Philippines dominated the list for all the wrong reasons. Manila and Cebu ranked ahead of Ho Chi Minh City (32.3), Phnom Penh (31.4), and Hanoi (31.1).

Numbeo’s Property Prices Index by City 2026 in Southeast Asia | Screenshot from Numbeo

What does “price-to-income ratio” actually mean?

Numbeo calculates this by comparing the median price of an apartment against a household’s annual disposable income. In simple terms, it’s an estimate of how many years’ worth of income a typical household would need to buy a home. The higher the number, the less affordable housing becomes.

A ratio of 35.9 means that, theoretically, an average household in Manila would need nearly 36 years of its disposable income to afford a home. Cebu households would need almost 34 years.

Of course, real life is more complicated than a formula. Numbeo itself notes that the index doesn’t account for factors such as taxes, maintenance costs, different housing types, inherited wealth, or financial assistance from family. Still, the figures paint a sobering picture of just how steep the climb toward homeownership has become.

It’s a global problem

Housing affordability has become a growing concern worldwide. The Economist Intelligence Unit noted that years of elevated inflation, rising borrowing costs, and expensive construction materials have reshaped housing markets globally. Even in countries where prices have cooled, higher mortgage rates continue to squeeze would-be buyers.

In other words, young adults around the world are asking the same question: How are we supposed to buy homes when simply staying afloat already costs so much?

Now, the question is, are the prices high, or are we all just bad at spending money?

For some Filipinos, homeownership is still achievable. We see Internet strangers celebrating their new houses all the time (paired with encouraging messages of how we can do it, too). Maybe if we all stopped buying matcha lattes, blind boxes, and concert tickets, we’d all magically afford a house in a few years. So is it just a case of spending money on all the wrong things? The reality isn’t that simple.

People come from vastly different circumstances. Some inherit property or receive help from family. Others support parents and siblings. Some earn six figures, while others struggle with stagnant wages despite working full-time.

Financial discipline certainly matters. Saving consistently, avoiding unnecessary debt, and building healthy money habits can improve your chances. But affordability is also shaped by larger forces: wages that fail to keep pace with property prices, rising living costs, limited housing supply in urban centers, and an economy where even middle-income earners can find themselves priced out.

Homeownership remains a dream for many, not because of laziness or poor choices, but because the math simply doesn’t add up.

What can you do if buying a home still feels impossible?

The numbers can be discouraging. If you’re still recovering from the realization that a McFlurry now costs around P60 (this author still remembers when it was P25!), seeing a 35.9 price-to-income ratio certainly doesn’t help.

But it doesn’t mean you should give up entirely. What are some of the things you can control?

- Build an emergency fund before taking on long-term debt.

- Improve your earning potential through career growth, side hustles, or upskilling.

- Explore housing options outside major city centers, where prices may be lower.

- Take advantage of government housing programs if you’re eligible.

- Save and invest consistently, even if progress feels slow.

- Remember that renting isn’t a personal failure. For many people, it’s the more practical financial decision.

The reality is that the “dream house by 30” timeline sold to previous generations no longer reflects the experiences of many young Filipinos today. And maybe success doesn’t have to look exactly the same.

Owning a home remains a worthwhile goal if it’s something you genuinely want. But if you’re not there yet, you’re not automatically irresponsible, immature, or “behind” in life. Let’s just do the best we can with the cards we’ve been dealt.

This article was originally published on 8List.ph.

Follow Windowseat.ph on Facebook, Instagram, and Tiktok for more relevant guides and information for better travel and commute experiences!

GUIDE: Full List of Ninoy Aquino International Airport Terminal Assignments

Previous

GUIDE: Full List of Ninoy Aquino International Airport Terminal Assignments

Previous

PSA: The Legendary Mandarin Oriental is Reopening in Makati this 2026

Next

PSA: The Legendary Mandarin Oriental is Reopening in Makati this 2026

Next